July 1, 2026

General

Freya Grant

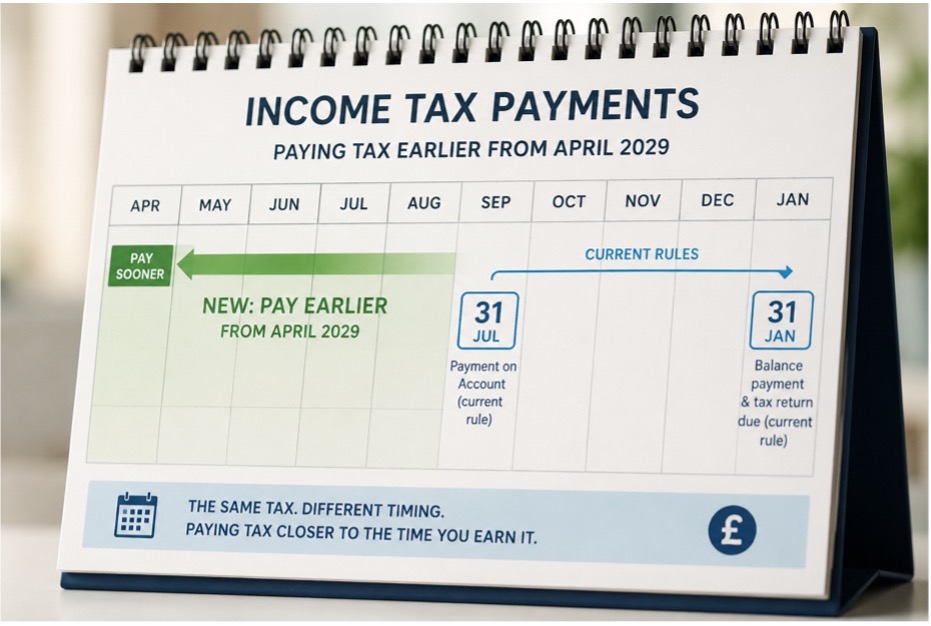

The government has launched a consultation on proposals to reform the Income Tax Self-Assessment (ITSA) payment system. If implemented, the changes would require many taxpayers to pay their income tax much earlier than they do under the current rules, with any reforms expected to take effect from April 2029.

The proposals aim to modernise the tax system by collecting income tax closer to the time income is earned, rather than many months after the end of the tax year.

Current rules

Under the existing Self-Assessment regime, individuals are generally required to file their tax return and pay any tax due by 31 January following the end of the tax year.

Many taxpayers are also required to make Payments on Account, which are advance payments towards the following year’s tax liability. These are typically due on 31 January and 31 July and are calculated using the previous year’s tax bill. Once the tax return has been submitted, any difference between the tax paid and the tax actually due is settled through a balancing payment or repayment.

The proposed changes

The consultation contains two separate proposals depending on how an individual pays tax.

Self-Assessment through PAYE

From April 2029, individuals who pay tax through both PAYE and Self-Assessment may have their Self-Assessment liabilities collected automatically through payroll deductions.

The amount deducted would initially be based on the taxpayer’s most recent available tax return, although taxpayers would be able to update their estimated income where circumstances change to better reflect their expected liability.

The government is also seeking views on whether additional safeguards should be introduced to protect taxpayers whose PAYE income changes during the year or is insufficient to cover the required deductions.

Earlier Payments on Account

For taxpayers who are not able to pay through PAYE, the government is considering significant reforms to the current Payments on Account regime.

Although no final approach has been decided, the consultation explores replacing the existing twice-yearly payment schedule with more frequent monthly or quarterly payments. The aim is to align tax payments more closely with when income is received.

Importantly, the consultation recognises that many taxpayers have irregular or fluctuating income and is seeking feedback on how any new system could accommodate changing income levels without creating unfair payment obligations.

What could this mean?

While the proposals would not increase the amount of tax payable, they would substantially alter when that tax is paid.

Individuals who currently benefit from the gap between earning income and paying the associated tax may need to review their cashflow planning if earlier payment dates are introduced. This is likely to be particularly relevant for those with variable income, including business owners, landlords and self-employed individuals.

Comment

Against the backdrop of ongoing pressure on the UK’s public finances, it is perhaps unsurprising that the government is considering reforms designed to accelerate the collection of income tax.

Although the proposals remain at the consultation stage, they represent one of the most significant potential changes to the Self-Assessment payment timetable in recent years. The extended lead-in period until April 2029 should give taxpayers and employers time to prepare, while also allowing the government to refine the proposals following consultation.

The consultation closes on 4 August 2026. We will continue to monitor developments and provide updates as further details become available.